Introduction

As we reach the midpoint of the decade, the manufacturing industry is undergoing a profound transformation. Once defined by mechanical scale and linear supply chains, manufacturing in 2025 is being reimagined through digital infrastructure, AI integration, sustainability goals, and workforce evolution. Global supply chain restructuring, domestic reshoring efforts, and heightened geopolitical uncertainties have made adaptability a central imperative. This comprehensive report delves into the 2025 landscape in depth, highlighting key sub-industries, regional performance, financial forecasts, supply chain dynamics, digital trends, sustainability priorities, and emerging risks.

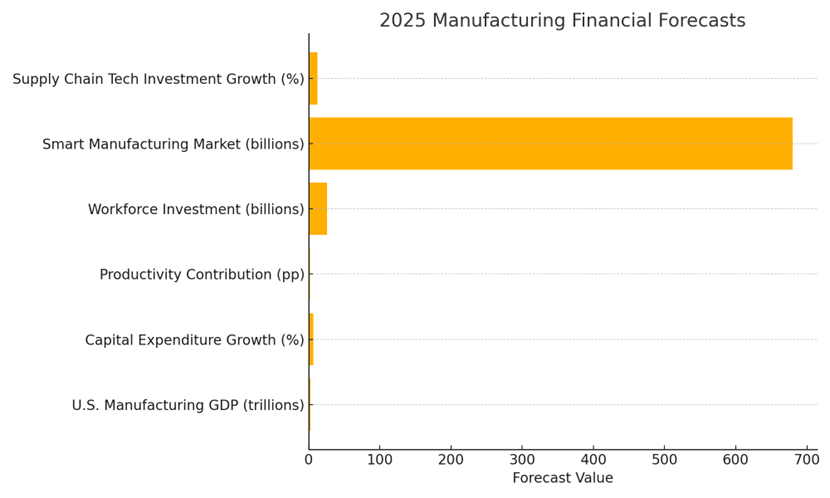

Financial Forecasts (2025)

The chart above highlights core financial projections that will shape the manufacturing economy in 2025, including GDP growth, capital expenditure increases, productivity gains from digital operations, and significant investments into workforce development and smart technologies.

The chart above highlights core financial projections that will shape the manufacturing economy in 2025, including GDP growth, capital expenditure increases, productivity gains from digital operations, and significant investments into workforce development and smart technologies.

Manufacturing Sector Comparison (2025)

| Sub-Industry | Key Trends | 2025 Growth Outlook |

| Automotive | EV expansion, automation, digital twins | Strong (40% EV capacity growth) |

| Aerospace & Defense | Supply chain resilience, additive manufacturing | Moderate (defense & commercial aviation demand) |

| Electronics & Semiconductors | CHIPS Act investment, AI/edge computing | High (7.5% revenue growth) |

| Food & Beverage | Sustainability, robotics, clean-label production | Stable (sustainability-driven) |

| Industrial Equipment | Predictive maintenance, cobots, MRO AI | Strong (public infra and private capex) |

Sub-Industry Deep Dive

Automotive Manufacturing

The automotive sector in 2025 is accelerating its shift toward electrification, digitalization, and sustainability. EV production capacity in North America alone is projected to expand by more than 40% through 2026. Automakers are reconfiguring legacy plants to accommodate electric drivetrains, optimizing operations through digital twins, and leveraging AI in both product development and plant logistics.

Robotic systems and AI-driven conveyor lines are improving production precision, enhancing safety, and enabling flexible production capabilities. Battery supply chains are being reshaped through vertical integration and onshoring efforts in response to rare earth material volatility. Government incentives and stricter emissions regulations continue to accelerate green transformation in the industry.

Aerospace & Defense

Aerospace and defense manufacturers are benefiting from a resurgence in both commercial and military demand. U.S. defense spending is expected to exceed $849 billion in FY2025, bolstering production pipelines and innovation funding. Additive manufacturing plays a growing role in rapid prototyping and maintenance applications, while real-time telemetry is driving performance-based logistics.

AR-enhanced training and predictive maintenance tools are being used to offset skilled labor shortages. Sustainability is also gaining attention with lightweight composite materials and more efficient jet engines that reduce fuel use and carbon emissions.

Electronics & Semiconductors

Projected to reach $697 billion in 2025, the semiconductor industry is thriving due to the explosive demand for computing power, connectivity, and automation. AI chips, edge processors, and sensors for IoT devices are central to this boom. The CHIPS Act in the U.S. is funding massive expansions in domestic fabrication capacity, aiming to reduce reliance on Asian supply chains.

Manufacturers are deploying AI in chip design, fab optimization, and predictive yield analysis. Clean energy-powered fabs and water recycling systems are also becoming standard, as sustainability and reliability take center stage in high-tech manufacturing.

Regional Outlook

United States

The United States remains a dominant force in global manufacturing, supported by policy, capital investment, and a skilled industrial base. In 2025, public incentives like the CHIPS Act and the Inflation Reduction Act are transforming the landscape of domestic manufacturing. New regional hubs are emerging across the Southeast (electric vehicles), Midwest (advanced materials), and Southwest (semiconductors).

Over $230 billion in construction spending was recorded in 2024 alone, and continued growth is expected through 2025. While manufacturing output dipped slightly with ISM reporting a PMI of 49.0 in mid-2025, growth in high-tech and clean-energy sectors is expected to buoy the industry in the second half of the year.

Canada & Mexico

Canada and Mexico are key partners in North American manufacturing. Mexico has become a primary nearshoring destination for electronics and automotive suppliers, benefiting from reduced tariffs, competitive labor, and proximity to U.S. markets. Canada, meanwhile, is advancing leadership in clean technologies and sustainable manufacturing.

Strategic trade alliances and logistical integration across the USMCA region are improving cross-border supply chain efficiency, enabling distributed manufacturing models and leaner operations.

Europe

European manufacturers in 2025 are accelerating their digital and environmental transformation. Germany, the Netherlands, and Nordic countries lead in smart factory implementation, while Eastern Europe benefits from cost-competitive labor and infrastructure investment. High energy prices remain a concern, pushing investment into renewables and energy-efficient operations.

EU directives on ESG transparency and supply chain emissions are creating higher compliance standards, prompting investments in monitoring technologies, traceability, and cleaner production systems.

Asia-Pacific

While China remains a manufacturing powerhouse, rising labor costs and trade friction are causing global firms to diversify operations to Vietnam, India, and Malaysia. Japan and South Korea continue to lead in precision electronics and robotics, with government-backed initiatives accelerating AI and IoT deployment in factories.

India’s ‘Make in India’ strategy is yielding strong results in electronics, pharmaceuticals, and renewable energy equipment, attracting foreign investment and expanding export capacity.

Latin America

Manufacturers in Latin America—particularly in Brazil and Colombia—are seeing moderate growth in agriculture processing, bio-manufacturing, and light industrial production. However, infrastructure gaps, regulatory fragmentation, and digital lag remain barriers to scale and integration with global supply chains.

Workforce and Talent Outlook

The talent gap remains one of the most pressing challenges in manufacturing for 2025. Deloitte and The Manufacturing Institute estimate that the U.S. will face a shortage of 1.9 million manufacturing workers by 2033, with nearly half of open roles in advanced manufacturing expected to go unfilled. The reasons are multifaceted: digital skill gaps, an aging workforce, and persistent misperceptions about manufacturing careers.

To close this gap, companies are ramping up investments in apprenticeships, certifications, and partnerships with technical schools and community colleges. In 2025, over 90% of manufacturers report having at least one talent pipeline collaboration in place. Upskilling programs are focusing on data analytics, AI interfacing, equipment maintenance, and digital safety protocols. AR/VR training systems and simulator-based certifications are now used to accelerate onboarding and reduce training time by up to 40%.

Supply Chain Strategy and Resilience

Supply chain modernization remains a top priority in 2025. Nearly five years after COVID-19 exposed deep vulnerabilities, manufacturers are embracing agile, digital, and diversified supply chain strategies. Persistent cost pressures and geopolitical risk have prompted a shift toward nearshoring, friend-shoring, and regionalization of production.

Smart logistics solutions powered by AI, machine learning, and IoT sensors are enabling real-time tracking and demand forecasting. Digital twins and blockchain-enabled transparency systems are providing end-to-end visibility. Autonomous supply chains are on the rise, using predictive data to automate routing, inventory management, and procurement decisions, reducing stockouts and optimizing throughput.

Sustainability and Environmental Innovation

Sustainability is no longer a marketing priority; it’s a regulatory and strategic imperative. ESG compliance is driving transformation at every level of operations. Manufacturers are targeting reductions in water, energy, and raw material usage, and embracing circular economy models that emphasize reuse, recycling, and refurbishment. Deloitte reports that IoT-enabled systems are capable of reducing energy consumption by up to 18% and material waste by up to 15%.

Major OEMs are deploying lifecycle analytics tools, digital carbon dashboards, and AI-driven emissions management systems. Green facilities powered by renewables and built with sustainable materials are increasingly common. Furthermore, companies are integrating ESG into supplier scorecards, ensuring that sustainability metrics cascade across their value chains.

Geopolitics and Industrial Policy

Global manufacturing in 2025 continues to be influenced by trade policy, tariffs, and the evolving regulatory landscape. U.S.-China tensions and export controls have triggered a global re-evaluation of supplier bases. In response, governments are funding strategic manufacturing capabilities—such as semiconductors, critical minerals, and renewable infrastructure—to boost national resilience.

Domestically, the Inflation Reduction Act (IRA) and the CHIPS Act are funneling billions into clean energy and semiconductor industries. However, policy uncertainty, especially around future tariffs and tax incentives, remains a challenge. Many firms are preparing dual-track contingency plans to mitigate risk from policy swings and global elections.

Conclusion

The 2025 manufacturing landscape is not merely adapting; it is evolving into a more dynamic, digitally integrated, and strategically decentralized ecosystem. Manufacturers are operating in an era where agility, intelligence, and sustainability are not just competitive advantages but operational necessities. The convergence of AI, cloud computing, edge technology, and autonomous systems is redefining how goods are designed, produced, delivered, and serviced. These innovations are unlocking unprecedented productivity gains and setting new standards for operational excellence across sectors.

Supply chain volatility, labor shortages, environmental pressures, and policy uncertainty continue to test the resilience of manufacturers. Yet the industry response has been proactive: digital twins, real-time logistics, smart facilities, and regional production hubs have all gained ground as long-term strategic solutions. The sector is witnessing an intentional shift toward transparency, traceability, and energy efficiency, driven by both market demands and regulatory frameworks.

Perhaps the most significant shift is cultural. The perception of manufacturing is changing from dirty and dangerous to clean, connected, and highly skilled. Companies that lean into this narrative by investing in workforce development, technology, and employer branding will be best positioned to attract the next generation of engineers, technicians, and data-driven decision makers.

Moving forward, success in manufacturing will require more than just capital and capacity. It will require vision. Vision to build smarter supply chains. Vision to rethink what sustainable production looks like. Vision to create inclusive talent ecosystems. And a vision to transform every factory floor into a platform for innovation. Those who commit to that path in 2025 will not only survive the volatility of today but define the industrial leadership of tomorrow.